Paper Trails Don't Lie — But They Can Be Burned

Why Manual Operations Are a Fraud Magnet

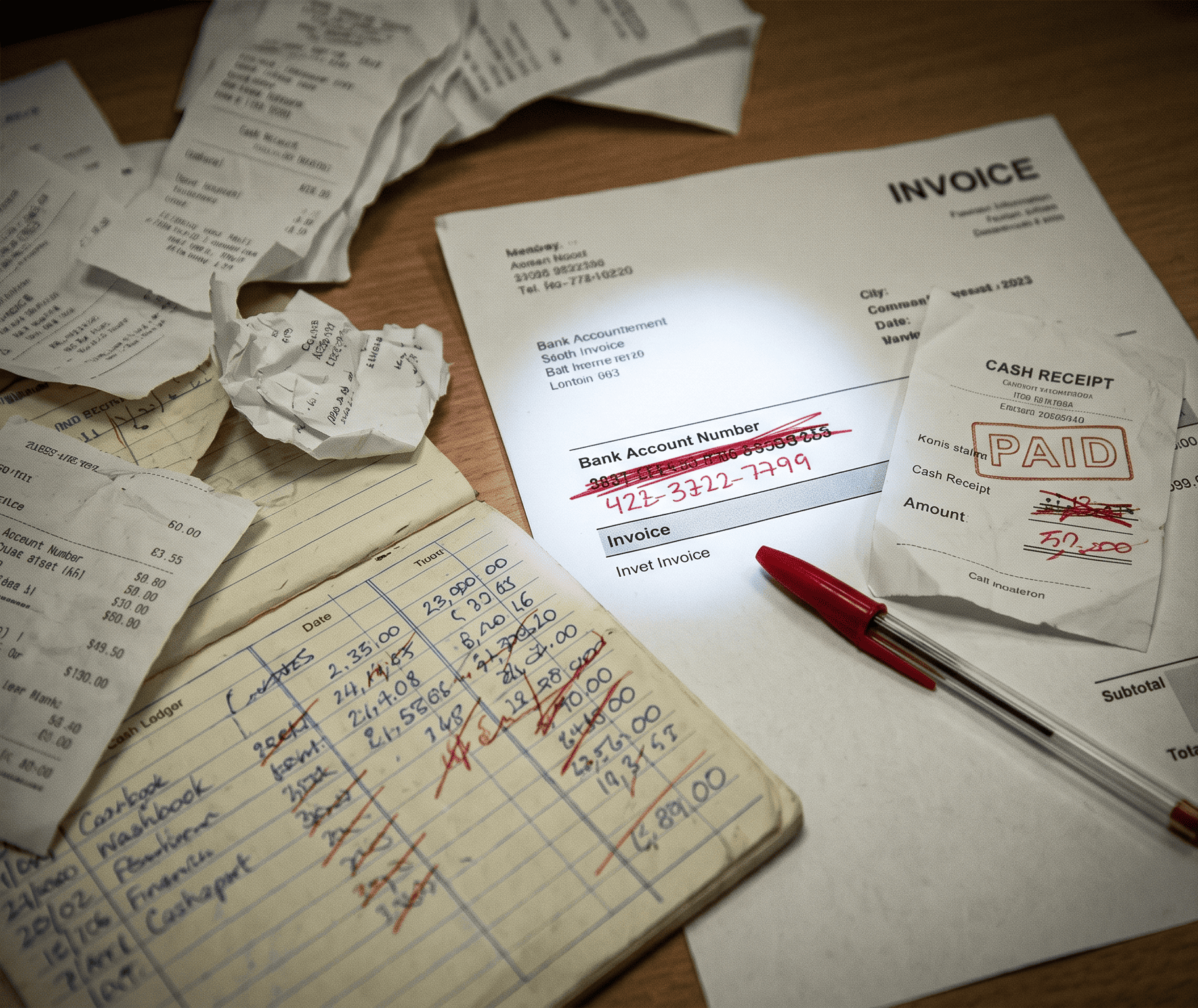

The invoice looks normal. Same supplier name, similar amount, familiar format. Nobody checks because nobody has time to cross-reference a spreadsheet against a physical file stored in a drawer across the office. By the time someone notices the bank account number changed, the money is gone.

This is not a rare scenario. It plays out in schools, clinics, logistics companies, and NGOs every single month — and the common thread is almost always the same: processes that run on paper, WhatsApp threads, and shared spreadsheets that nobody fully controls.

The Data Is Clear

The Association of Certified Fraud Examiners (ACFE) publishes a biennial study on occupational fraud, drawing on thousands of real cases from 138 countries. The 2024 edition, covering over 1,900 investigated cases, surfaced a finding that should concern every operations manager running a manual shop: more than half of all occupational fraud cases occurred because of either a lack of internal controls or someone overriding the controls that existed.

The typical fraud scheme ran for 12 months before it was caught. The median loss per case was $145,000. The typical organization loses an estimated 5% of annual revenue to fraud — and that figure is conservative, because it only counts what gets detected.

Smaller organizations — the schools, clinics, and SMEs that make up the bulk of Nigeria's institutional economy — were found to have higher fraud exposure as a percentage of revenue than large ones, precisely because they are less likely to have the controls and audit structures that bigger firms maintain.

Why Manual Operations Are Structurally Vulnerable

Fraud does not require a criminal mastermind. It requires opportunity. And manual, non-digitized operations hand opportunity out freely, in three specific ways.

1. No Audit Trail

When a transaction happens on paper, the record of it exists only as long as the paper does — and only as accurately as the person who filled it in. There is no system logging who created a record, who changed it, and when. A fraudster working within a manual system can alter, delay, or simply not record a transaction, and the gap may never surface unless someone physically reconciles every document by hand.

In a digitized system, every action leaves a timestamped record. Deletion attempts are logged. Approvals are tracked. The very existence of this trail deters a significant portion of fraud before it starts — because the opportunity to hide it is gone.

2. One Person Holds the Keys

Manual operations concentrate knowledge and access. One person maintains the fee ledger. One person tracks supplier payments. One person reconciles the petty cash. When that person is the only one who understands the system, oversight becomes nearly impossible.

The ACFE data confirms this pattern: fraud is significantly more likely where a single individual controls multiple steps of a financial process without independent verification. In a digitized environment, separation of duties — where approving, recording, and reconciling a transaction are handled by different accounts — can be enforced at the system level. In a manual environment, it is enforced only by goodwill and management attention, which is an unreliable safeguard.

3. Detection Lags by Design

Manual processes are slow. Reconciliation happens at the end of the month. Audits happen at the end of the year. By the time an anomaly surfaces, the pattern has been running long enough to do real damage.

The ACFE study found that fraud schemes detected through automated controls had significantly lower losses than those discovered through tips or by accident — because automation can flag the anomaly the day it happens, not 12 months later.

What This Looks Like in Practice

Consider a mid-sized private school managing fees manually. Tuition payments come in as cash or bank transfers. A bursar records each payment in a register. There is no system cross-checking the register against the bank statement in real time.

A small, consistent discrepancy — recording a partial payment as a full one, skimming a fixed amount from cash receipts — can run for an entire academic year before it shows up in an annual audit. At $500 per month, that is $6,000 gone before anyone notices. At $2,000 per month across multiple streams, the exposure is significant.

The same logic applies to a clinic recording patient consultations on paper, or an NGO tracking program expenses in a shared Excel file with no version control and no approval workflow. The gap between what happened and what was recorded is where fraud lives.

The Objection Worth Addressing

Some organizations resist digitization on cost grounds. Software is expensive, implementation is disruptive, staff need training, and the system might not fit the way the organization actually works.

These are real concerns, and they deserve a serious answer rather than a dismissal.

The cost of a proper operations system — even a custom-built one designed around how the organization actually runs — is a one-time investment. The cost of fraud is recurring, often undetected, and frequently unrecoverable. The ACFE found that 51% of organizations that experienced fraud were unable to recover the funds lost. Of those that recovered something, nearly two-thirds recovered less than 25 cents on the dollar.

The question is not whether the organization can afford to digitize. It is whether it can afford not to.

What Good Controls Actually Look Like

Digitization is not the same as buying expensive software and hoping for the best. The goal is a system that makes these five things true:

Every transaction is recorded automatically at the point it happens — not manually entered later by a single person with unchecked discretion.

Every record carries a clear ownership trail — who created it, who approved it, who last modified it.

Approvals require more than one person for anything above a defined threshold — so no single individual can authorize and process a payment alone.

Reconciliation runs continuously, not monthly — so discrepancies surface in days, not at year-end.

Reports are generated by the system, not manually compiled — so the report itself cannot be manipulated before it reaches management.

None of this requires enterprise-grade software with a six-figure implementation budget. A well-built system designed around the organization's actual workflows — its fee categories, its supplier list, its staff roles — can deliver all five at a fraction of the cost of a year's worth of undetected fraud.

The Bottom Line

Fraud is not primarily a character problem. It is a systems problem. Most people who commit fraud at work were not planning to when they started. They found an opportunity, they took it, and they took it again because nothing flagged it.

The organisations that get defrauded least are not the ones with the most virtuous staff. They are the ones that have designed their operations so that fraud is hard to commit, hard to hide, and quick to surface.

That design starts with getting processes off paper.

Orderly Problem Solvers (OPS) builds custom management systems for schools, clinics, and other B2B organisations in Nigeria. If your administrative processes still run on spreadsheets and paper — and you want to understand what a digitised alternative actually involves — get in touch.